Near-term challenges notwithstanding, a young demographic base, growing income levels and expanding middle-class, along with many first-time homebuyers in the millennial age group, will favourably impact demand for housing in India, in the years to come.

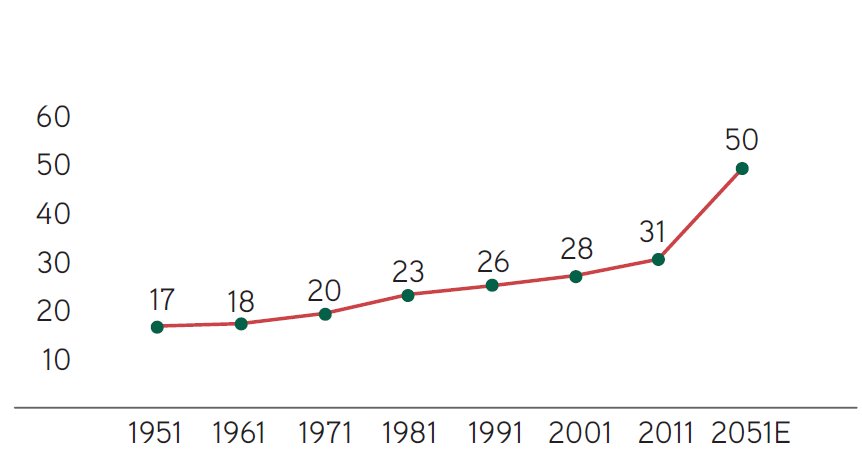

RAPID URBANISATION

The number of towns and cities in recent years has dramatically increased and this growth is expected to continue. According to a United Nations report, half of India’s population would be living in urban areas by 2030. The Government has outlined massive infrastructure investments to ensure efficient functioning, including housing, road network, transport, water supply, electricity and other related infrastructure. This includes creation of Smart Cities and the ‘Housing for All’ scheme, to support the development of mass urban housing infrastructure.

Rate of urbanisation in India, 1951-2051E (%)

Source: NHB's report on trend and progress of housing in India, 2018.

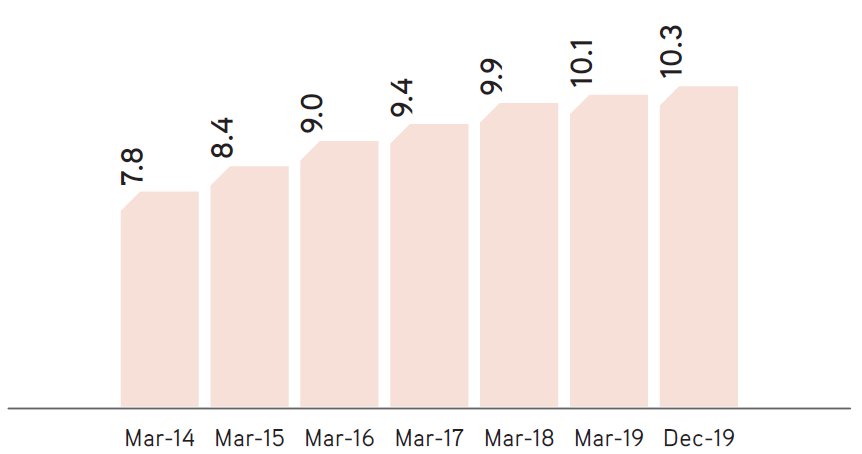

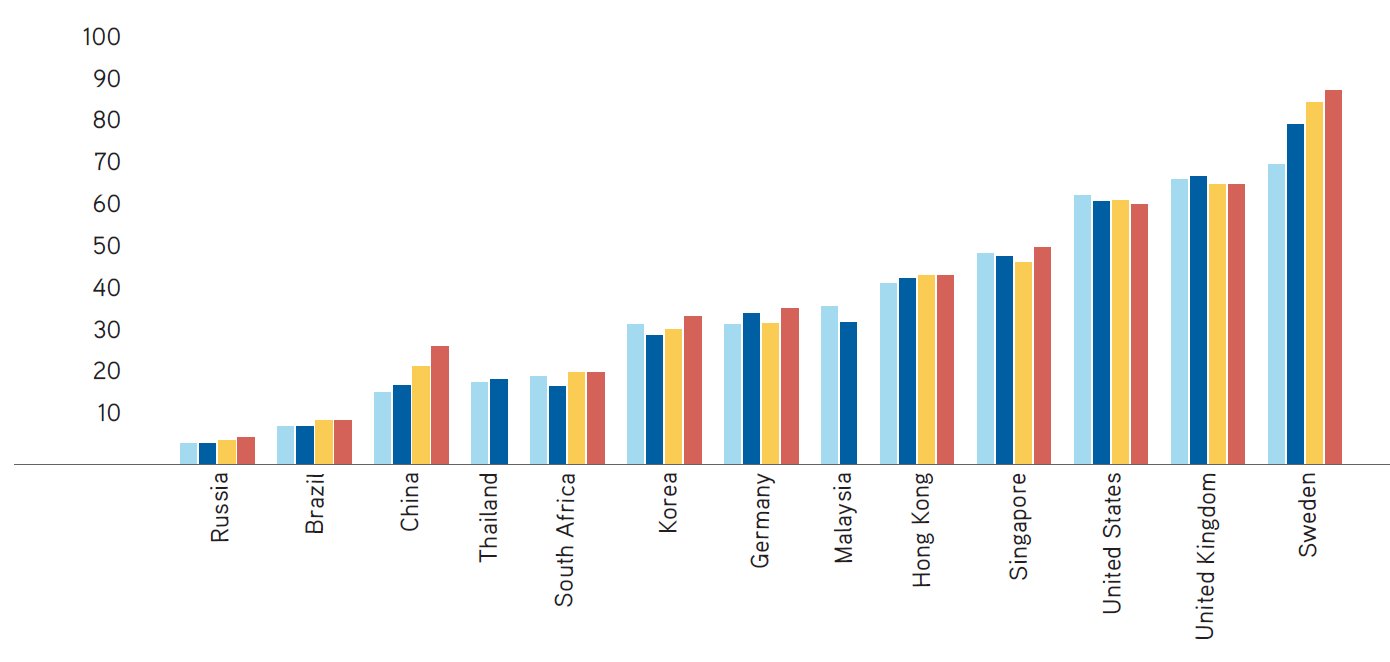

UNDERPENETRATED MORTGAGE MARKET

According to the Reserve Bank of India (RBI), India’s mortgage-to-GDP ratio stands at nearly 10%, as compared with 18% in China, 52% in Singapore and 56% in the US. With the ratio expected to rise to 12% by 2022, it would still remain significantly below that of its developed and developing peers, which points to significant headroom for mortgage market growth over the longer term.

Housing credit trends in India (%)

Note: Housing credit as a % of GDP

Source: ICRA report on the Indian mortgage finance market, April 2020

Housing credit trends for various countries around the world (%)

Note: Housing credit as a % of GDP

Source: ICRA report on the Indian mortgage finance market, April 2020

ACUTE SHORTAGE IN HOUSING

India faces a significant shortage in housing, which is expected to increase with growing population. Despite sustained Government policy focus, the shortage is much more pronounced in the economically weaker and lower income segments. The emergence of specialised HFCs, with innovative lending models and underwriting processes has started to democratise house ownership, which is likely to accelerate further and drive growth in the mortgage market.

Projected housing requirement by 2022

| Analyst estimate | GoI estimate | |

| Shortage and requirement (million) | ||

| EWS | 33.6 | 45.0 |

| LIG | 44.0 | 50.0 |

| MIG and above | 6.4 | 5.0 |

| Total | 80.0 | 100.0 |

| Value of units, LTV to be financed by HFCs, SCBs (` lakh crores) | ||

| EWS | 25.2 | 33.8 |

| LIG | 88.0 | 100.0 |

| MIG and above | 51.2 | 40.0 |

| Total | 164.4 | 173.8 |

| Total (` lakh crores) | 2.3 | 2.5 |

| Construction costs (` lakh crores) | ||

| EWS | 26.9 | 36.0 |

| LIG | 55.0 | 62.5 |

| MIG and above | 19.2 | 15.0 |

| Total | 101.1 | 113.5 |

| Total (` lakh crores) | 1.4 | 1.6 |

Note: EWS - Economically Weaker Section; LIG - Low Income Group; and MIG - Middle Income Group

Source: Planning Commission, analyst estimates